Introduction

The global commodity trade and chemical industry find themselves at a historical turning point. The future of this sector will be shaped by an intersection of powerful structural, geopolitical, and technological factors. The industry must face a prolonged downcycle, which is driven on the one hand by global oversupply (including especially massive exports from China), and on the other hand – by weakening demand, regulatory uncertainty, and the radical restructuring of supply chains in the face of international tensions.

To build an advantage before the arrival of the next recovery cycle, market leaders will have to act on multiple tracks. The key to success and margin defense will become rigorous capital protection, portfolio restructuring with a strong shift towards specialty chemicals, and continuous investments in innovation (R&D). In this complex ecosystem, artificial intelligence will play the role of a key process optimizer. The ultimate winners – forming, as the McKinsey & Company report terms it, a global group of the „privileged few” – will however be those organizations that most effectively combine modern technologies with three market foundations: free access to capital, control over physical commodity flows, and high resilience to geopolitical shocks.

Macroeconomic background

The chemical industry, instead of the expected rebound, has bogged down in a prolonged downcycle. Initial forecasts for 2025 assumed a global production growth of 3.5%, however reality verified these plans – revised estimates point to 1.9% in 2025 and barely 2% in the year 2026.

Instead of stabilization, markets are facing unprecedented uncertainty driven by three main factors:

- Slowing economy: Global GDP is projected to grow by barely 3.0% (2025) and 3.1% (2026), with a simultaneous slowdown of momentum in the USA to 1.8% and 1.4% respectively.

- Geopolitics and trade wars: Conflicts in the Middle East and in Europe are paralyzing supply chains. As a result, it is forecasted that in 2025 the volume of US chemical imports will fall to the 2020 level, and exports – to the lowest values since 2021.

- Regulatory instability: While the EU eases part of the sustainability requirements (e.g., through the 6th Omnibus simplification package), and the CBAM mechanism begins to protect the internal market, the United States dynamically alters its own regulations, which drastically impacts the financial models of planned projects.

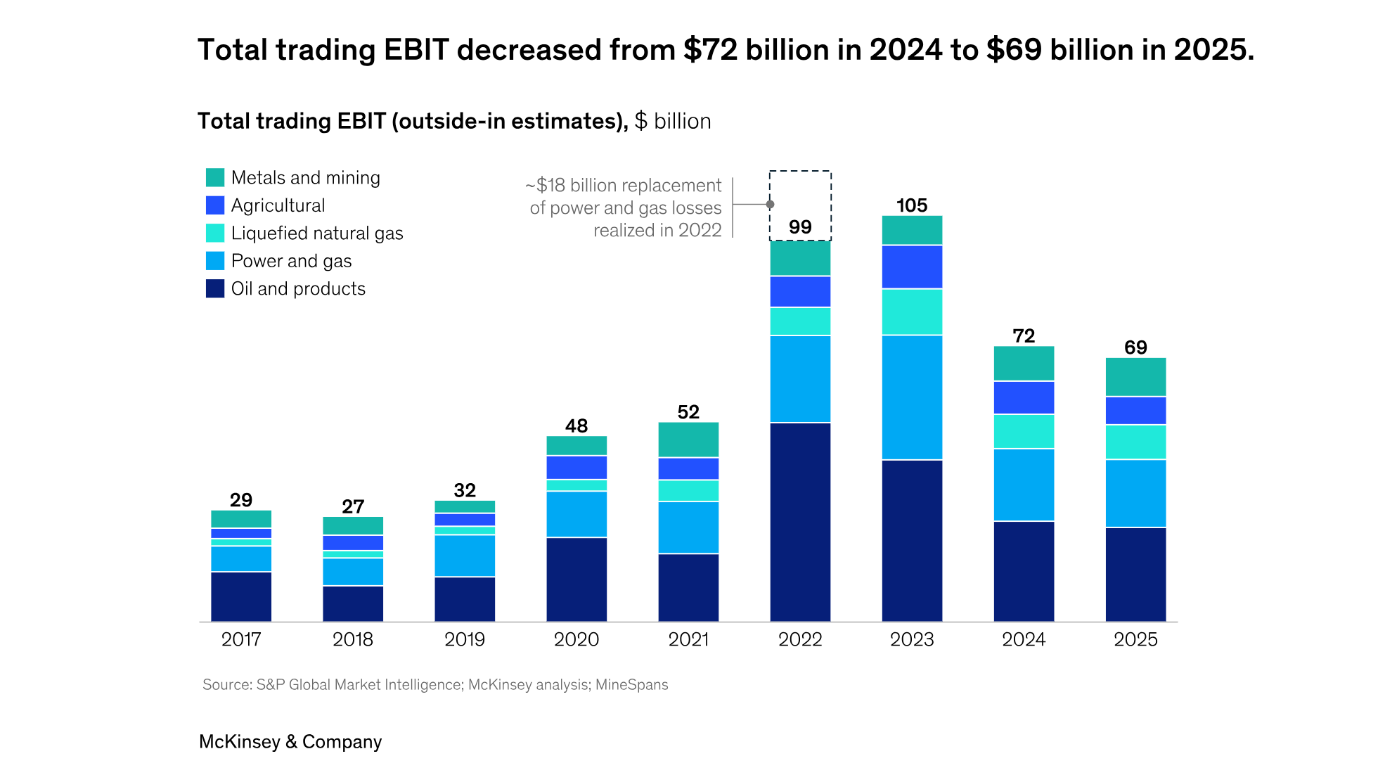

The difficult situation is confirmed by hard data: EBIT profit in global trading shrank from $72 billion in 2024 to $69 billion in 2025. This means that the total pool of profits generated across the entire industry decreased by about 5%. Lower market volatility, combined with political uncertainty, distinctly limited the opportunities for achieving above-average profits, particularly in the European power market.

Source: https://www.mckinsey.com/industries/energy-and-materials/our-insights/at-the-threshold-of-a-new-era-in-commodity-trading „At the threshold of a new era in commodity trading”

Structural challenges and regional disparities

Commodity markets are currently characterized by very limited flexibility, which makes them extremely susceptible to external shocks. Building resilience, especially in the area of critical raw materials for the energy transition (lithium, cobalt, nickel), is a slow process – creating alternative supply chains often takes a whole decade. Similar diversification challenges affect the oil, gas, and agriculture sectors.

The main problem of global chemistry, however, is not solely weak demand, but a massive oversupply of a structural nature. China, after saturating the internal market, flooded the West with cheap raw materials, which drastically lowers the margins of European and American plants.

Europe finds itself in the worst situation. The main problem of global chemistry, however, is not solely weak demand, but a massive oversupply of a structural nature, which is directly pointed out by S&P Global analysts. China, after the slowdown of the internal construction boom, shifted its modern, gigantic plants to export. As market analyses show, including among others the „2026 Chemical Industry Outlook” report developed by Deloitte, cheap Chinese raw material is currently flooding Western markets, triggering drastic price pressure and a ruthless erosion of margins for European and American plants.

The effects of this phenomenon are confirmed by hard market data: in the face of the flood of cheap chemicals from Asia, the utilization of production capacities in Europe fell to a disturbingly low level of about 74.6%.

The combination of gas prices three times higher than in the USA and aggressive competition from Asia is, however, not everything. The European industry is suffocating under the weight of rigorous environmental regulations. While the United States deregulates the market, and China focuses on maximizing production, European producers must face costly reporting requirements (e.g., the CSRD directive) and emission fees. Although the European Commission is trying to save the situation with a simplification package (the so-called 6th Omnibus), and the CBAM mechanism is ultimately intended to protect the market from high-emission imports, the current regulatory pressure drastically raises the operational costs of local plants.

This glaring cost uncompetitiveness has led to a wave of dramatic business decisions. Industry reports by experts, such as the European Chemical Industry Council (Cefic) and Roland Berger, indicate that since 2022, installations accounting for 9% of total production capacities have been closed on the Old Continent (which represents a loss of 37 million tons). The final effect of this structural import pressure is the permanent loss of 20,000 direct jobs in the European chemical industry.

Defense and seeking strategic business niches

To survive in the era of new volatility, enterprises must adapt their operations to key market trends:

- Rigorous profit prioritization: As market analyses show (including among others the „2026 Chemical Industry Outlook” report by Deloitte), enterprises are forced to rationalize assets and defend liquidity. A clear geographical division is outlined here: while in the USA and Qatar – where, as experts emphasize, the advantage is access to cheap feedstocks (primarily cheap natural gas and ethane derived from it) – new ethylene and polyethylene production plants will be launched in 2026, Europe, suffocated by high costs, will continue the painful process of closing factories and divestments.

- Making supply chains more flexible: Agile responding to tariff wars and the volatility of freight costs becomes essential.

- End-demand management: The chemical sector is highly dependent on construction and automotive, which record cyclical declines. Companies must therefore balance risk.

- Continuous innovations: Effective investing in research and creating new, unique products is today the only way for companies to not have to compete with rivals solely on the lowest price.

- Aggressive AI adoption: The use of artificial intelligence for operational transformation is no longer an option, but a market requirement.

Innovations as a protective shield: R&D and digitalization

Despite the ongoing downcycle, industry leaders do not give up on innovations. Instead of cutting budgets for the development of products and digital models, they treat them as an essential element of building resilience and fleeing forward. This opens doors to new markets and allows responding to changing consumer needs. This transformation covers four main areas:

- Revolution in operating models: Along with the rapid evolution of end markets and digital technologies, companies must redefine the way of delivering value. This requires a thorough audit and restructuring of talent management, processes, as well as partnership policies and corporate governance.

- Tailor-made products: Advancing commoditization ruthlessly cuts margins in base chemistry. The escape from this phenomenon is focusing on specialty chemistry. Instead of minor, incremental improvements, companies must develop breakthrough solutions that precisely respond to hitherto unmet market needs.

- Process optimization: A rigorous revision of operational and commercial processes allows squeezing the maximum out of available resources. Modern technologies help to radically cut energy consumption, minimize the amount of waste, and raise the overall efficiency of production.

- Intelligent sales and marketing: Customer expectations are shifting towards advanced experiences based on measurable value. Data analytics combined with artificial intelligence allows companies to personalize offers and build significantly more effective sales strategies.

Cost pressure blocked the mergers and acquisitions market (in the first half of 2025, only 243 transactions were recorded – the fewest since pre-pandemic years). It is predicted, however, that the currently ongoing revision of portfolios will trigger a strong wave of consolidation shortly after 2026. Producers will mass transition towards the aforementioned specialty chemistry, for which growth forecasts reach an optimistic 5–6.3%.

Source: https://www.deloitte.com/us/en/insights/industry/chemicals-and-specialty-materials/chemical-industry-outlook.html „2026 Chemical Industry Outlook”

Semiconductors: A golden niche in the era of slowdown

Despite general stagnation, the development of data centers powering artificial intelligence has created a gigantic niche for the chemical sector. The global semiconductor market is expected to grow by 8.5% in 2026, overcoming the barrier of $760 billion and heading towards the value of $1 trillion in 2030 (half of which will constitute AI chips).

Since specialty chemicals constitute from 9% to 14% of the material costs of electronics, the industry is also reacting to this trend. Since the beginning of 2025, we have been observing a rash of multi-million greenfield investments in the production of ultra-pure solvents and gases. They are to secure supply chains for the newly emerging chip factories in Europe and the USA (the reshoring trend).

Examples:

- Air Liquide investment in Europe (Germany): At the end of 2024 / beginning of 2025, the French gas giant Air Liquide announced an investment worth over 250 million euros in the construction of new production units in Dresden (in the heart of the so-called „Silicon Saxony”). This is the largest investment in the company’s history supporting the electronic industry in Europe. The plant will produce ultra-pure nitrogen, oxygen, hydrogen, and argon to directly (on-site) power the newly emerging European chip factories (in Dresden, a gigantic factory is being built among others by the ESMC consortium, which includes Taiwanese TSMC, Bosch, and Infineon).

- Strategic Air Liquide plants in the USA (Idaho and New York): The same concern (Air Liquide) recently announced the construction of a completely new production installation in the state of Idaho in the USA (an investment of the order of over $250 million). The goal is to supply industrial gases of the highest purity for the new memory chip factory being built by Micron Technology. Additionally, the company allocated another $50 million for the expansion of infrastructure supplying ultra-pure nitrogen for GlobalFoundries factories in the USA.

- Fujifilm expansion in Europe (electronic materials): At the beginning of 2025, the Japanese concern Fujifilm (and more precisely its European company FUJIFILM Electronic Materials) announced further multi-million capital investments in the expansion of its production capacities on the Old Continent (the company owns plants among others in Belgium, France, and in Italy). The company’s authorities explicitly argue this move with the necessity of „local securing of supplies for local demand” (the reshoring trend) and drastic shortening of supply chains for European semiconductor producers.